1

Please refer to important disclosures at the end of this report

1

1

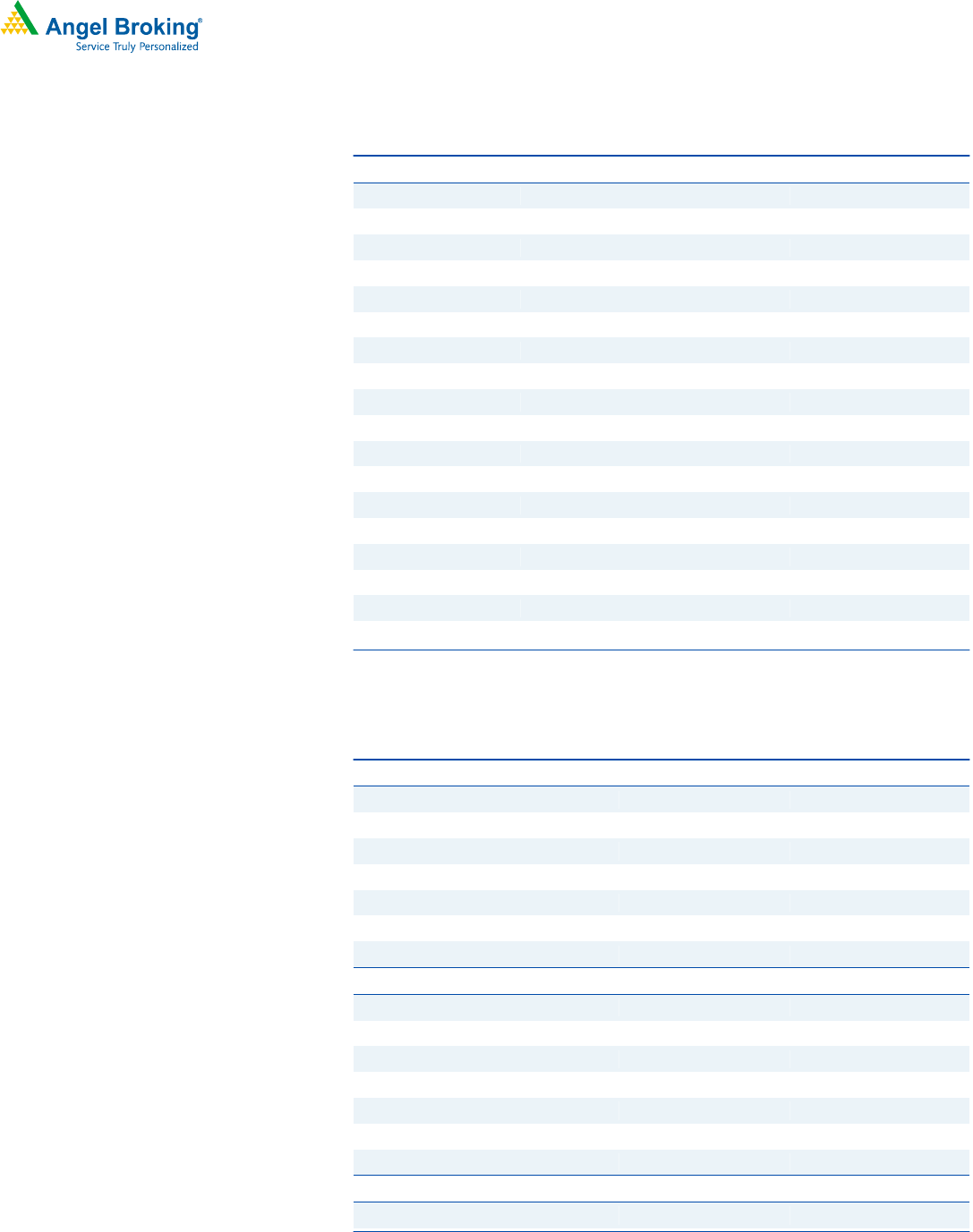

Particulars (` Cr)

Q2FY20

Q1FY20

% chg (qoq)

Q1FY20

% chg (yoy)

NII

6,102

5,844

4

5,232

17

Pre-prov. profit

5,952

5,893

1

4,094

45

PAT

(106)

1,370

-

790

-

Source: Company, Angel Research

For Q1FY2020, Axis Bank reported loss of `106Cr primarily driven by one time

impact of deferred tax asset of `2,140Cr and higher provision of `3,512Cr

(Against Estimation of `2,063Cr). The key positives for the quarter were, increase

in pre-provision profit by 45% yoy and domestic loan growth by 19% yoy coupled

with an improvement in NIM.

Provision and slippages remained elevated: Higher slippages (3.8%) and credit

cost (2.7%) coupled with no clarity on watch list outside the BB & Below book

declared in Q1FY2020 (`6,700Cr) marred the performance of Q2. Out of the

total slippages of `4,983Cr, `2,862Cr slipped from corporate book and 97% is

from BB & Below book (`1,920Cr pertains to loan and `940Cr to investment

book). Notably, in Q1FY20, the management had given a new list of potential

stressed loans in 8 stressed corporate groups. Total exposure to above corporate

was `12,200Cr, of which exposure worth `6,700Cr is not part of BB & below

book, however no clarity has been in Q2FY2020. Nevertheless, the bank has

taken additional contingent provision worth `2,600Cr. We expect banks credit

cost to remain on higher side till overall stressed asset (BB&B book & Stressed

asset declared in Q1FY20) recognise as NPA.

Jump in other income, contained Opex aids pre-provision profit: During the

quarter, other income jumped by 45% yoy led by treasury gain worth `809Cr. The

key driver of core fee income growth was Retail fees, which grew 16% yoy and

constituted 64% of the Bank’s total fee income. Card fees grew strongly by 21%

yoy. Opex grew at 6% yoy aided by rationalisation of outsourced services, digital

initiatives and lower promotion spends. Management expects Opex to remain

contained for FY2020.

Retail loans drive momentum; NIM improves: During Q2FY2020, the bank’s

advances grew by 14% yoy, led by retail, up 23% yoy. However, overseas book

de-grew 25% yoy. Domestic NIMs improved by 11bps yoy to 3.51%.

Management guided NIM for FY2020 in the range on 3.5-3.8%. Deposit grew at

a healthy rate of 22% yoy; however, CASA grew 5% yoy. CASA ratio plunged by

660bps/22bps yoy/qoq to 41.1%, however other banks are also witnessing

decline in CASA ratio.

Outlook & Valuation: Axis Bank currently trades at 2x its FY2021E price to book

value (after adjusting value of subsidiaries). We expect the stock to get re-rated

owing to (1) new leadership, (2) receding stressed loan pool, and (3)

improvement in return ratios (ROA/ROE – 1.5%/15% by FY2021E). We

recommend Buy on the stock with a Target Price of `860.

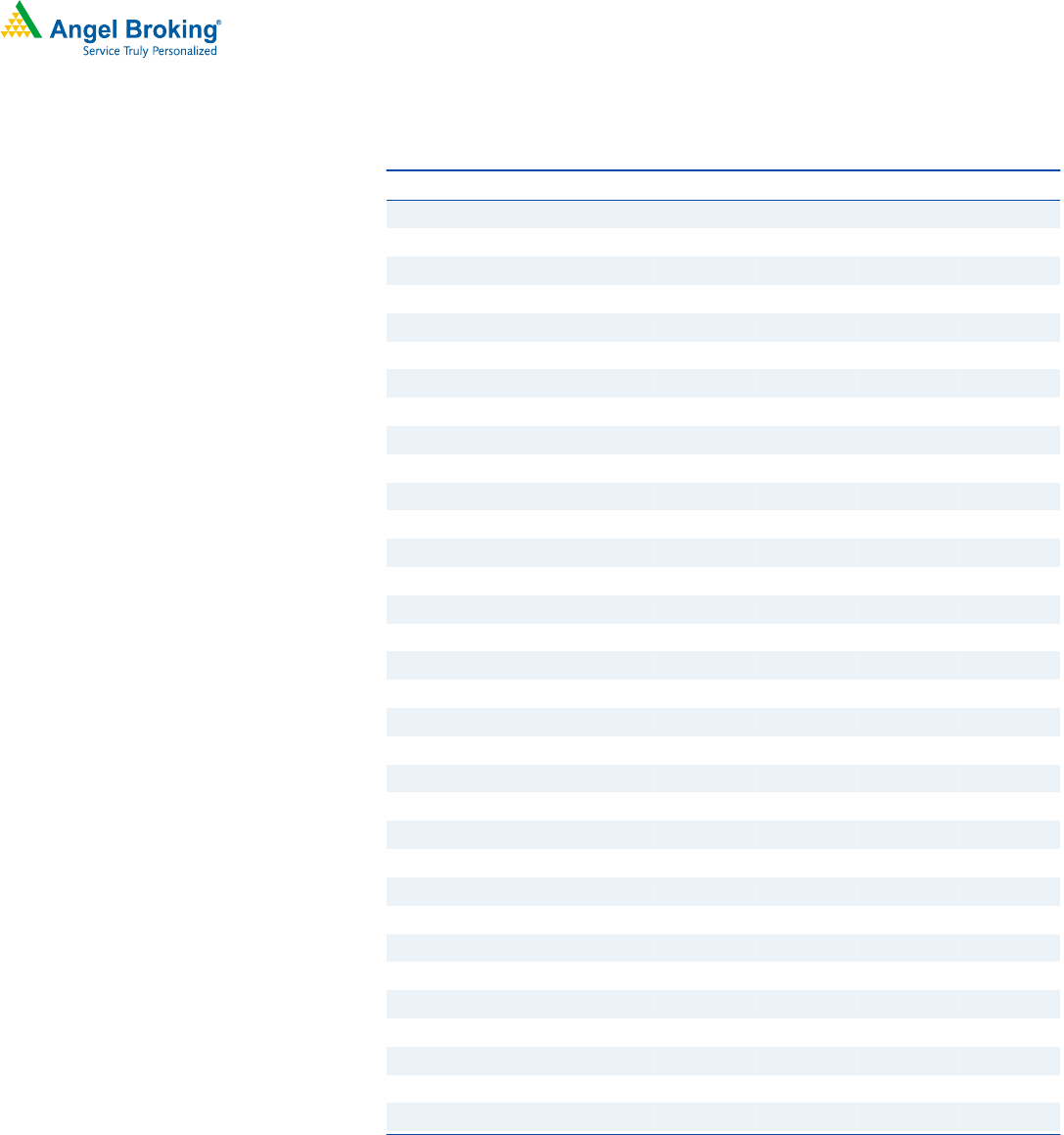

Exhibit 1: Key Financials

Y/E March (` cr)

FY17

FY18

FY19

FY20E

FY21E

NII

18,093

18,618

21,708

24,940

30,040

% chg

7

3

17

15

20

Net profit

3,679

276

4,677

6,626

14,465

% chg

-55

(93)

1,596

42

118

NIM (%)

3.4

3.1

3.2

3.2

3.3

EPS (`)

13

1

17

24

51

P/E (x)

24

55

730

43

30

P/ABV (x)

3.8

3.8

3.5

3.2

2.3

RoA (%)

0.6

0.0

0.6

0.8

1.5

RoE (%)

7

0.5

7

8

15

Source: Company, Valuation done on closing price of 23/10/2019

BUY

CMP `714

Target Price `860

Investment Period 12 Months

Stock Info

Sector

Bloomberg Code

Shareholding Pattern (%)

Promoters 16.2

MF / Banks / Indian Fls 22.2

FII / NRIs / OCBs 47.1

Indian Public / Others 12.2

Abs. (%) 3m 1yr 3yr

Sensex 1.6 13.5 40.1

Axis Bank (2.3) 26.8 (6.7)

Nifty

11,604

Reuters Code

AXBK.BO

AXSB IN

Face Value (`)

2

BSE Sensex

39,058

52 Week High / Low

827/543

Avg. Daily Volume

2,71,058

Beta

1.3

Banking

Market Cap (` cr)

2,00,923

3-year price chart

Source: Company, Angel Research

200

400

600

800

Oct-16

Feb-17

Jun-17

Oct-17

Feb-18

Jun-18

Oct-18

Feb-19

Jun-19

Oct-19

Axis Bank

Strong operating performance; Slippages elevated

Q2FY2020 Result Update | Banking

Oct 24, 2019

2

Axis Bank|Q2FY2020 Result Update

Oct 24, 2019

2

Exhibit 1: Quarterly Performance

Particulars (` cr)

Q1FY19

Q2FY19

Q3FY19

Q4FY19

Q1FY20

Q2FY20

% chg (qoq)

% chg (yoy)

Interest Earned

12,777

13,281

14,130

14,798

15,255

15,438

1

16

on Advances / Bills

9,612

9,955

10,628

11,127

11,461

11,924

4

20

on investments

2,682

2,802

2,894

2,971

3,119

2,868

(8)

2

on bal with RBI & others

125

162

183

224

192

195

2

21

on others

358

363

424

476

483

451

(7)

24

Interest Expended

7,610

8,049

8,526

9,092

9,411

9,336

(1)

16

Net Interest Income

5,167

5,232

5,604

5,706

5,844

6,102

4

17

Other Income

2,925

2,678

4,001

3,526

3,869

3,896

1

45

Operating income

8,092

7,910

9,604

9,232

9,712

9,998

3

26

Operating Expenses

3,720

3,816

4,080

4,217

3,820

4,046

6

6

Employee expenses

1,228

1,175

1,203

1,142

1,307

1,275

(2)

9

Other Opex

2,492

2,642

2,877

3,075

2,513

2,771

10

5

Pre.Prov Profit

4,372

4,094

5,525

5,014

5,893

5,952

1

45

Provisions & Contingencies

3,338

2,927

3,055

2,711

3,815

3,512

(8)

20

PBT

1,034

1,167

2,470

2,303

2,078

2,440

17

109

Provision for Taxes

333

377

789

798

708

2,545

259

575

Tax rate

32

32

32

35

34

104

206

223

PAT

701

790

1,681

1,505

1,370

(106)

-

-

Balance sheet

Advance (` Cr)

4,41,074

4,56,121

4,75,105

4,94,798

4,97,276

5,21,594

5

14

Deposit (` Cr)

4,47,079

4,79,680

5,14,092

5,48,471

5,40,678

5,83,958

8

22

Credit-to-Deposit Ratio (%)

99

95

92

90

92

89

(265.2)bp

(576.8)bp

CA (` Cr)

68,278

80,128

84,172

89,265

71,211

79,138

11

(1)

SA (` Cr)

1,41,359

1,48,742

1,51,380

1,54,129

1,52,263

1,60,916

6

8

CASA deposits (` Cr)

2,09,637

2,28,870

2,35,552

2,43,394

2,23,474

2,40,054

7

5

CASA %

47

48

46

44

41.3

41.1

(22.4)bp

(660.5)bp

CAR (%)

15

15

15

15

16.1

18

239bp

333bp

Tier 1 CAR (%)

12

12

12

11

12.9

14

114bp

233bp

Profitability Ratios (%)

Yield Advance

8.73

8.88

9.13

9.18

9.24

9.23

(1.4)bp

35.1bp

COF REPO

5.23

5.34

5.44

5.69

5.70

5.6

(8)bp

28bp

Reported NIM - Domestic

3.50

3.59

3.61

3.61

3.56

3.6

7bp

4bp

Cost-to-income ratio

0.46

0.48

0.42

0.46

0.39

0.40

1.1bp

(7.8)bp

Asset quality

Gross NPAs (` Cr)

32,662

30,938

30,855

29,789

29,405

29,071

(1)

(10)

Gross NPAs (%)

6.52

5.96

5.75

5.26

5.25

5.03

(22)bp

(93)bp

Net NPAs (` Cr)

14,902

12,716

12,233

11,276

11,037

11,138

(2)

(26)

Net NPAs (%)

3.09

2.54

2.36

2.06

2.04

2

(5)bp

(55)bp

PCR (%)

53

57

59

61

61

60

(70.5)bp

305.5bp

Slippage ratio (%)

1.0

0.6

0.8

0.6

1.0

1.0

(1)bp

34.7bp

Credit Cost on Adv

0.8

0.6

0.6

0.5

0.8

0.7

(9.4)bp

3.2bp

Source: Company, Angel Research

3

Axis Bank|Q2FY2020 Result Update

Oct 24, 2019

3

Exhibit 2: Advance

Particular (` Cr)

Q1FY19

Q2FY19

Q3FY19

Q4FY19

Q1FY20

Q2FY20

% chg (qoq)

% chg (yoy)

Retail

211648

221710

232397

245812

258205

273223

6

23

Home Loan

84659

86467

90635

93409

98118

101093

3

17

Rural Lending

29631

28822

32536

34414

30985

35519

15

23

Auto Loan

23281

24388

25564

27039

30985

32787

6

34

PL

21165

24388

25564

29497

30985

32787

6

34

LAP

16932

19954

18592

22123

20656

24590

19

23

CC

8466

8868

11620

12291

12910

13661

6

54

SBB

6349

6651

6972

7374

10328

10929

6

64

Other

21165

22171

20916

19665

23238

21858

(6)

(1)

Corporate Banking

172443

174149

180469

183402

177455

187000

5

7

Term Loan

121948

119520

124698

1,21,122

119379

1,27,096

6

6

WC

50495

54629

55771

62,279

58076

59,904

3

10

SME

56983

60262

62238

65584

61616

61371

(0)

2

Term Loan

12348

12496

12846

13,475

12757

13,047

2

4

WC

44635

47766

49392

52,109

48859

48,324

(1)

1

Total

441074

456121

475104

494798

497276

521594

5

14

Source: Company, Angel Research

Exhibit 3: GNPA Movement

Particular

Q3FY18

Q4FY18

Q1FY19

Q2FY19

Q3FY19

Q4FY19

Q1FY20

Q2FY20

GNPA Opening

27,402

25,001

34,249

32,662

30,938

30,855

29,790

29,406

Fresh Slippage

4,428

16,536

4,337

2,777

3,746

3,012

4,798

4,983

Slippage (%)

1.1%

3.8%

1.0%

0.6%

0.8%

0.6%

1.0%

1.0%

Slippage Annual

4.2%

15.0%

3.9%

2.4%

3.2%

2.4%

3.9%

3.8%

Upgrade & Recovery

4,008

3,401

2,917

2,186

1,622

2,376

2,177

2,213

Write off

2,821

3,887

3,007

2,315

2,207

1,701

3,005

3,104

Closing GNPA

25,001

34,249

32,662

30,938

30,855

29,790

29,406

29,072

Provision

13,232

17,657

17,760

18,222

18,622

18,513

18,367

17,933

NPA

11,769

16,592

14,902

12,716

12,233

11,277

11,039

11,139

Prov

2,811

7,180

3,338

2,927

3,055

2,711

3,815

3,512

Credit Cost (%)

0.7%

1.6%

0.8%

0.6%

0.6%

0.5%

0.8%

0.7%

CC Ann (%)

2.7%

6.5%

3.0%

2.6%

2.6%

2.2%

3.1%

2.7%

Source: Company, Angel Research

4

Axis Bank|Q2FY2020 Result Update

Oct 24, 2019

4

Exhibit 4: Non-NPL stress declared in Q1FY20

Particular (` cr)

Q1FY20

BB & Below rated loans as on1QFY20

7,504

Non-Fund based stress pool (NFB to BB & Below & NPLs)

2,500

Security Receipt

2,940

Total of existing stress (1)

12,944

New list (After removing overlap)

New loan addition (Exposure 7,000cr and 3,900cr considered in NPA & BB & Below)

3,100

New Non-Fund based addition (Actual 3,000cr and 1,000cr considered in NPA)

2,000

New Investment addition (Exposure 2,200cr and NPA/MTM taken 200cr/400cr)

2,000

Total of new list (2)

7,100

Total stress on loans (1)+(2)

20,044

Provisions on non-NPL stress

2,358

Total stress loans

17,686

Total stress loans (%)

3.56

Source: Company

Exhibit 5: SOTP

Sum of the parts

Stake in Company%

Valuation

Methodology

Value/Share `

Core Business

100.0

2.4x FY21E ABV

836

Axis Capital Ltd

100

15x FY21E PAT

9.1

Axis MF

75

20x FY21E PAT

3.9

Axis Fin

100

1.5x FY21E Book Value

9.8

Axis Sec

100

15x FY21E PAT

4.9

holding value post 20% disc

22.1

Sum of Parts

860

Source: Company, Angel Research, Valuation done on closing price of 23/10/2019

5

Axis Bank|Q2FY2020 Result Update

Oct 24, 2019

5

Income Statement

Y/E March (` cr)

FY17

FY18

FY19E

FY20E

FY21E

Net Interest Income

18,093

18,618

21,708

24,940

30,040

- YoY Growth (%)

7

3

17

15

20

Other Income

11,691

10,967

13,130

15,457

17,347

- YoY Growth (%)

25

(6)

20

18

12

Operating Income

29,784

29,585

34,839

40,396

47,388

- YoY Growth (%)

14

(1)

18

16

17

Operating Expenses

12,200

13,990

15,833

17,339

19,799

- YoY Growth (%)

21

15

13

10

14

Pre - Provision Profit

17,585

15,594

19,005

23,058

27,589

- YoY Growth (%)

9

(11)

22

21

20

Prov. & Cont.

12,117

15,473

12,031

11,375

8,259

- YoY Growth (%)

227

28

(22)

(5)

(27)

Profit Before Tax

5,468

122

6,974

11,683

19,330

- YoY Growth (%)

-56

(98)

5,637

68

65

Prov. for Taxation

1,788

(154)

2,297

5,057

4,865

- as a % of PBT

33

(127)

33

43

25

PAT

3,679

276

4,677

6,626

14,465

- YoY Growth (%)

(55)

(93)

1,596

42

118

Balance Sheet

Y/E March (` cr)

FY17

FY18

FY19E

FY20E

FY21E

Equity

479

513

513

524

524

Reserve & Surplus

55,284

62,932

66,676

88,969

1,02,711

Net worth

55,763

63,445

67,190

89,493

1,03,235

Deposits

4,14,379

4,53,623

5,48,471

6,36,227

7,50,748

- Growth (%)

16

9

21

16

18

Borrowings

1,05,031

1,48,016

1,52,776

1,60,415

1,76,456

Other Liab. & Prov.

26,387

26,373

28,733

15,985

18,946

Total Liabilities

6,01,559

6,91,458

7,97,169

9,02,119

10,49,384

Cash Balances

30,858

35,481

35,099

45,641

46,349

Bank Balances

19,398

7,974

32,630

13,159

15,426

Investments

1,28,793

1,53,876

1,74,969

2,00,132

2,28,648

Advances

3,73,069

4,39,650

4,94,798

5,73,966

6,77,279

- Growth (%)

10

18

13

16.0

18

Fixed Assets

3,747

3,972

4,827

5,599

6,607

Other Assets

45,693

50,505

54,847

63,623

75,075

Total Assets

6,01,559

6,91,458

7,97,169

9,02,119

10,49,384

- Growth (%)

11

15

15

13

16

6

Axis Bank|Q2FY2020 Result Update

Oct 24, 2019

6

Key Ratio

Y/E March

FY17

FY18

FY19

FY20E

FY21E

Profitability ratios (%)

NIMs

3.43

3.13

3.16

3.18

3.34

Cost to Income Ratio

41

47

45

43

42

RoA

0.6

0.0

0.6

0.8

1.5

RoE

7

0

7

8

15

B/S ratios (%)

CASA Ratio

51.4

53.8

44.4

44.4

44.4

Credit/Deposit Ratio

90

97

90

90

90

Asset Quality (%)

Gross NPAs

5.04

6.77

5.0

4.0

3.8

Net NPAs

2.11

3.40

2.3

1.6

1.5

Credit Cost

3.2

3.5

2.4

2.0

1.2

Provision Coverage

0.58

0.50

0.54

0.60

0.61

Per Share Data (`)

EPS

13

1

17

24

51

ABVPS (70% cover.)

190

203

224

309

358

DPS

5

5

5

5

7

Valuation Ratios

PER (x)

24

55

730

43

30

P/ABVPS (x)

3.8

3.8

3.5

3.2

2.3

Dividend Yield (%)

0.6

0.7

0.7

0.7

0.7

DuPont Analysis

FY17

FY18

FY19E

FY20E

FY21E

NII

3.2

2.9

2.9

2.9

3.1

- Prov

2.1

2.4

1.6

1.3

0.8

Adj NII

1.0

0.5

1.3

1.6

2.2

Other Income

2.0

1.7

1.8

1.8

1.8

Total Income

3.1

2.2

3.1

3.4

4.0

Opex

2.1

2.2

2.1

2.04

2.0

PBT

1.0

0.0

0.9

1.4

2.0

TAX

0.3

-0.0

0.3

0.6

0.5

RoA

0.6

0.0

0.63

0.78

1.48

Leverage

10.5

10.8

11.4

10.8

10.1

RoE

6.8

0.5

7.2

8.5

15.0

Valuation done on closing price of 23/10/2019

7

Axis Bank|Q2FY2020 Result Update

Oct 24, 2019

7

Disclosure of Interest Statement Axis Bank

1. Financial interest of research analyst or Angel or his Associate or his relative No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives No

3. Served as an officer, director or employee of the company covered under Research No

4. Broking relationship with company covered under Research No

Ratings (Based on expected returns Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

over 12 months investment period): Reduce (-5% to -15%) Sell (< -15)

Research Team Tel: 022 - 39357800 E-mail: [email protected] Website: www.angelbroking.com

Angel Broking Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited, Bombay

Stock Exchange Limited, Metropolitan Stock Exchange Limited, Multi Commodity Exchange of India Ltd and National Commodity &

Derivatives Exchange Ltd It is also registered as a Depository Participant with CDSL and Portfolio Manager and Investment Adviser with

SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Limited is a registered entity with SEBI for Research

Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number INH000000164. Angel or its associates has not

been debarred/ suspended by SEBI or any other regulatory authority for accessing /dealing in securities Market. Angel or its

associates/analyst has not received any compensation / managed or co-managed public offering of securities of the company covered

by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavors to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.